The Rising Tide of Insurance Losses: Wildfires and Storms Shape Economic Impact in 2025

Extreme weather events are increasingly reshaping the landscape of insurance economics, as evidenced by the staggering $107 billion in insured losses reported globally in 2025. According to a recent analysis from Swiss Re, one of the leading reinsurance companies, the driving forces behind these losses were primarily wildfires and storms. Notably, wildfires alone wreaked havoc in Los Angeles, leading to unprecedented insured losses of $40 billion. While the overall losses in 2025 marked a decline from the previous year, this reduction was attributed more to fortuitous circumstances than to a genuine decrease in risk. The absence of major hurricanes making landfall in the United States significantly influenced this year's figures, highlighting the interplay between extreme weather events and economic ramifications in the insurance sector.

The data presented by Swiss Re is particularly alarming when considering the context of long-term trends. The report indicates that while insured losses dipped slightly from $137 billion in 2024, they have been on an upward trajectory, rising by an average of 5-7% annually since 1996 when adjusted for inflation. This trend underscores a growing vulnerability to natural disasters, with climate change acting as a catalyst that exacerbates the frequency and intensity of such events. Although the report refrains from explicitly linking these losses to human-induced climate change, the scientific community has long established that global warming significantly increases the likelihood and severity of extreme weather phenomena. The implications of this rise in losses extend beyond immediate economic concerns, impacting the sustainability and viability of insurance markets worldwide.

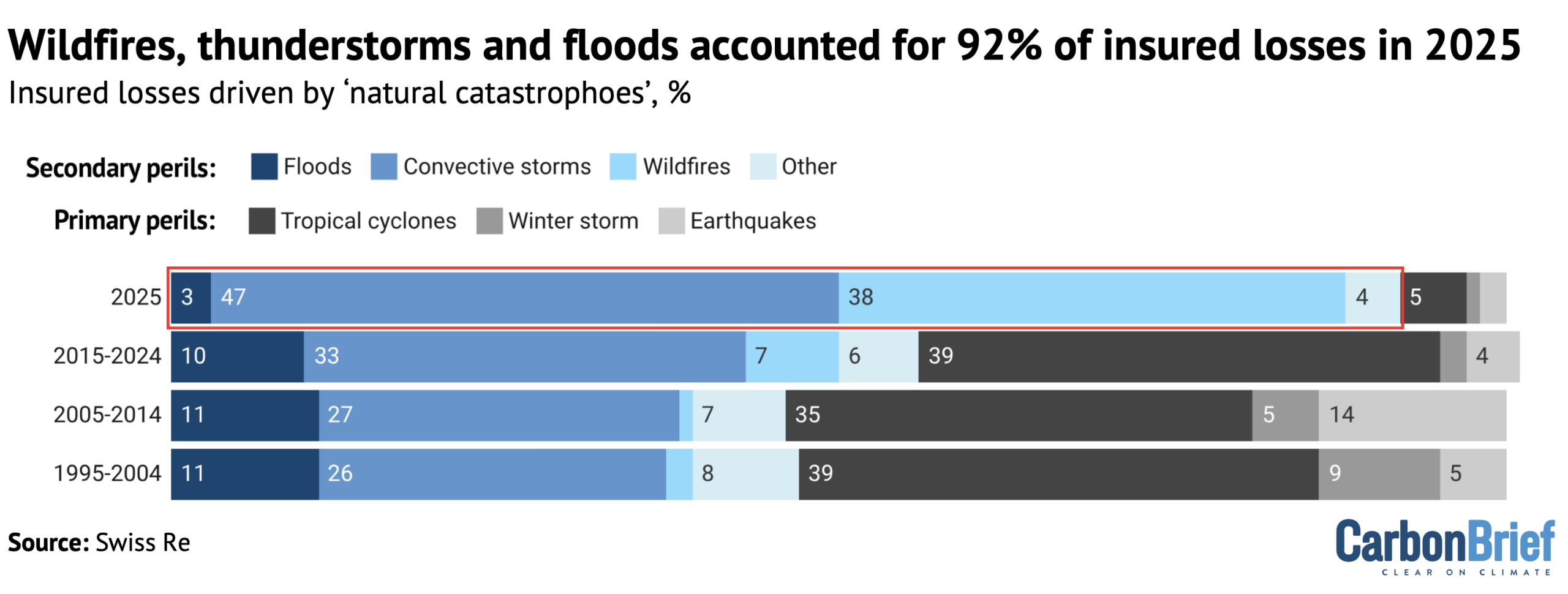

An analysis of the data reveals that secondary perils, events like wildfires, floods, and thunderstorms, accounted for a staggering 92% of the total insured losses in 2025. This figure represents a historic high, reflecting an increase from an average of 56% from 2015 to 2024. Secondary perils are generally more frequent but less damaging than primary perils, which include catastrophic events such as earthquakes and tropical cyclones. The growing share of secondary peril losses signals a significant shift in the risk landscape, underscoring the necessity for the insurance industry to adapt its models and risk assessments accordingly. The field of attribution science, which examines the influence of climate change on the frequency and intensity of weather events, plays a crucial role in understanding these shifts. As researchers continue to unravel the complex interconnections between climate change and natural disasters, insurers must recalibrate their approaches to remain viable.

The report also highlights the disparity in insurance coverage across different regions, particularly in emerging economies where a substantial gap exists in protection against climate-related losses. While insured losses in 2025 were lower than in prior years, the forecast for 2026 suggests a potential resurgence, with estimates ranging from $148 billion under normal circumstances to an alarming $320 billion if significant natural events occur. Notably, the absence of severe storms in the U.S. market, one of the largest and most robust insurance sectors, significantly impacted the overall loss calculations. Tropical cyclones, which have historically accounted for nearly 39% of insured losses from 2015 to 2024, contributed only 5% to losses in 2025. This stark contrast illustrates how localized events can have profound implications for global insurance trends.

Emerging from this analysis is a pressing need for the insurance industry to innovate and adapt to the changing climate. As Dr. Balz Grollimund, a leading figure in catastrophe model development at Swiss Re, emphasizes, ongoing review and adjustment of risk models are essential. The insurance sector must not only rely on historical data but also integrate evolving climate realities into their predictive frameworks. Improved modeling, combined with robust adaptation and mitigation strategies, is crucial to curtailing losses and ensuring that vulnerable regions remain insurable. The urgency for these adaptations cannot be overstated, as the growing frequency of extreme weather events continues to challenge the very foundations of risk assessment and economic stability in the insurance landscape.

Ultimately, the findings of the Swiss Re report serve as a clarion call for stakeholders across the insurance industry, policymakers, and the general public. The escalating trend of insured losses driven by climate-related disasters underscores the necessity for proactive measures to address the looming threats posed by climate change. As communities grapple with the immediate impacts of wildfires and storms, a broader, more holistic approach toward resilience and risk management must be established. The interplay between climate change, extreme weather events, and economic outcomes in the insurance sector is a complex but critical area of focus. Understanding these dynamics will be essential for crafting effective policies and fostering sustainable growth in a rapidly changing world.